Great Businesses Aren't Always Great Investments.

I wrote about quality being expensive a bit ago. Today, I want to go into more depth about why that matters.

There’s a lot of hype around “quality” and “compounders” right now. There’s a lot of willingness to pay high multiples for these businesses.

I see people using Warren Buffett’s transition from a ‘value’ investor to a ‘quality’ investor being used as justification to pay up for good companies.

It’s absolutely true that Charlie Munger helped Warren see the value in paying up for great businesses. Buffett gave Charlie credit in his shareholder letter this year for being the “architect” of Berkshire.

Everyone knows the quote, but I’ll put it in here anyway -

It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

— Warren Buffett

Couple that, with this:

‘Over the long term, it’s hard for a stock to earn a much better return that the business which underlies it earns. If the business earns six percent on capital over forty years and you hold it for that forty years, you’re not going to make much different than a six percent return – even if you originally buy it at a huge discount. Conversely, if a business earns eighteen percent on capital over twenty or thirty years, even if you pay an expensive looking price, you’ll end up with one hell of a result.’

– Charlie Munger

And we can pay a lot if the business is good enough, right? That depends on what you think of as “a lot.”

Price matters.

John Huber has a great framework about the 3 engines of value:

Here’s how I think about it. We can get returns on an investment from 3 places:

Earnings growth

Multiple expansion

Shareholder yield

Huber uses reduced share count for #3 in his framework, but I like shareholder yield. That takes into account reduction in share count through buybacks, return of capital through dividends, and I consider debt paydown shareholder yield as well.

Any increase in any of those 3 categories can make the value of a business go up. Any reduction can make it go down.

What’s a fair price?

There’s plenty of studies out there that show you can pay a higher multiple for a great business. Surely the Oracle of Omaha has read them. Surely he’s willing to pay up for great businesses. He bought Apple after all! Let’s look at that purchase.

Apple

Buffett bought Apple in the first half of 2016. It was around $25 a share most of that time.

Apple’s 2015 EPS was $2.31

That’s about 11x earnings. Not exactly expensive.

Let’s look at another recent purchase:

Occidental Petroleum

Bought initially in 2019 at $40 to $45 a share.

2018 EPS: $5.40

PE: 7.5 to 8.3

One more, and he really paid up for this one…

Chubb Limited

The most recent Berkshire purchase. Surely Buffett paid a lot - the Shiller PE is high, the Wilshire/GDP ratio is off the charts!

He initially started accumulating at the end of 2023, at $210 to $225.

2022 EPS: $12.40

PE: 16.9 to 18.2

Then he bought more in 2024, at around $260

2023 EPS: $21.80

PE: 11.9

What’s NOT a Fair Price?

Despite his evolution from value investor to quality investor, Buffett rarely pays more than 15x earnings, even for great businesses. Why? I’ll show you.

The next few examples are quite old, and the data gets a little funky due to splits and adjustments by different data providers. So, for EPS and share prices, I went back to the actual 10-K documents from the companies.

Microsoft in 2000

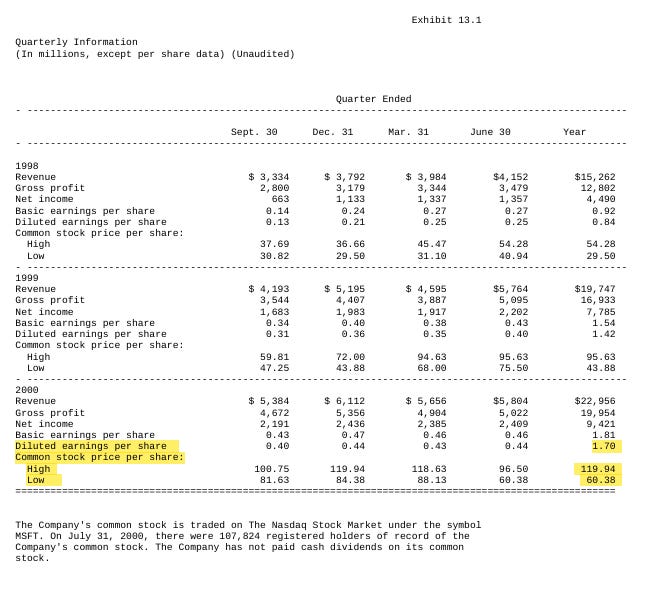

Microsoft was a great company in the 90’s and 2000’s, and it’s a great company today. Back then, it was so good that the government sued it for being a monopoly in 2001 and tried to break it up. How’d an investment in Microsoft do?

In 2000: $1.70 EPS

Stock traded between $60.38 and $119.94

PE of 35 to 70.5.

Buying somewhere near the peak in late 1999 or early 2000 meant that it took until 2016 for an investor to break even. Assuming you held on that long. Most probably didn’t.

Coke

Here’s a Warren Buffett favorite! He’s said that he should have sold Coke in 1998, but didn’t because of the massive size of his holding and the tax

1997 EPS: $1.64

Closed 1997 at $66.69, Buffett said it traded around $80.

PE of 40.7x to 48.8x

If you bought in 1998, you briefly broke even in 2012 and had a short window in 2013 to sell for some gain. Again, if you held.

“It was always a wonderful business, but clearly at 50 times earnings, it was a silly price on the stock.”

That’s what Buffett said about Coke in the video above.

Going back to the three engines of growth, Microsoft and Coke both grew earnings through the decade or more of zero returns.

But the multiple contracted so much that the stock went down.

There is a difference between a wonderful business and a wonderful investment.

I think a lot of investors get so caught up in “compounding” that they forget what they’re trying to compound.

Paying too much for a business that compounds its earnings for years can still be a bad investment.

We’re not looking for businesses that compounds earnings. We’re looking to compound our capital.

Buying a growing business at a fair price is one way to do that. But it’s not the only way.

What are today’s Mircosofts and Cokes?

I don’t know, but I can take some guesses.

Costco is a wonderful business.

Cintas is a wonderful business.

Constellation Software is a wonderful business.

But at 50, 46, and 102 times earnings, they might not be great investments.

Great post I couldn’t agree more! It’s a mistake I find a lot of newer investors fall for (myself included).

Nice work; thanks for drafting. The word "might," in your last sentence is doing some heavy lifting :-)