Semler Scientific

An article you weren't going to get.

I briefly looked at Semler Scientific about a week ago. I ruled it out pretty quickly and wasn’t even going to bother writing an article about it. But, they’ve made an announcement that has made them much more visible among the investing community.

So now, you’re getting an article about Semler that I wasn’t planning on writing on a day you wouldn’t normally get an article. Think of it as a bonus!

This is written in chronological order. The research I did is presented first, then we’ll talk about what’s got investors noticing Semler all of a sudden.

The Business

Until a few days ago, Semler Scientific was down almost 50% from it’s high prices this year. The spike up at the end is the result of that recent announcement I highlighted.

Semler is a healthcare company that are targeted at the early detection and treatment of chronic diseases.

Currently Semler’s only offering is QuantaFlo, a four-minute in-office blood flow test that is currently approved to detect asymptomatic peripheral artery disease (PAD).

That’s important because PAD is a precursor to lots of chronic diseases. Here’s a rundown according to Semler:

30% of people over 65 screen positive for PAD

The majority of them are not diagnosed because they’re asymptomatic.

1 to 2 years after a positive PAD test health risks increase:

All cause mortality – 20% higher risk

Major Adverse Cardiac Event (MACE) - >20% risk

Major Adverse Limb Event (MALE) - >Threefold risk

Health issues and cost of asymptomatic PAD are similar to that of symptomatic PAD

Catching something like PAD early and starting to make changes can really improve outcomes and save healthcare costs.

One of the major reasons that physicians don’t screen for PAD more is because it’s difficulty and time consuming:

QunataFlo changes that. It takes 4 minutes and can be done by medical staff in the office.

Sounds pretty good so far!

Profitability, Valuation, Etc.

They’ve been growing revenue and earnings:

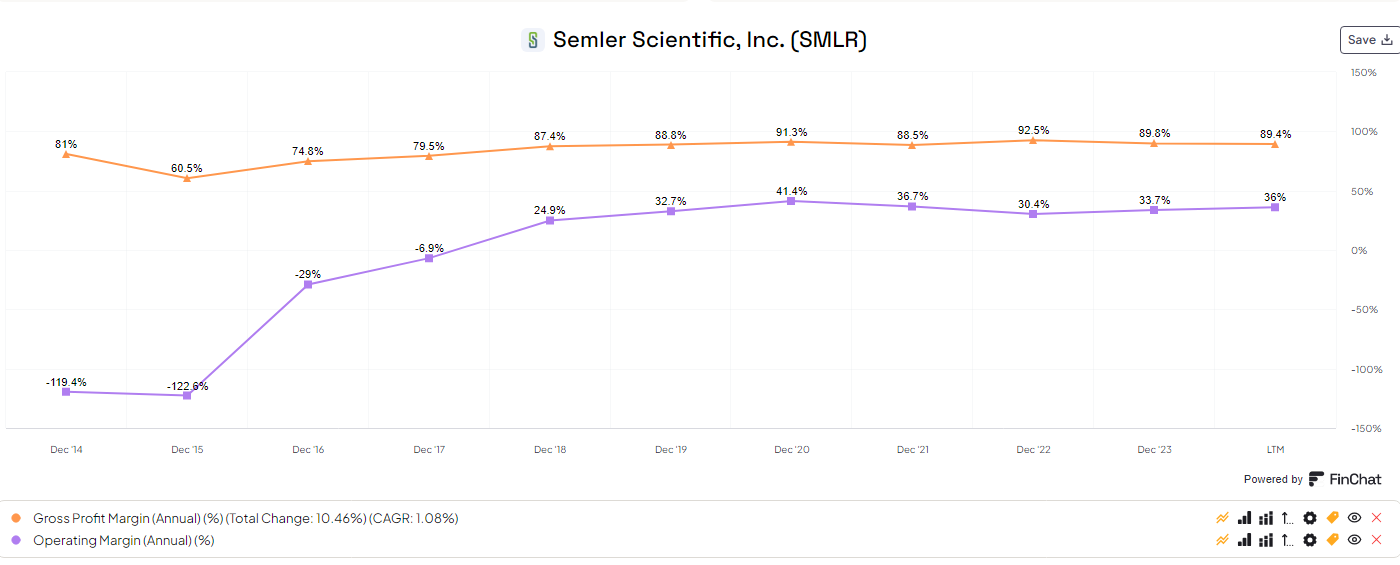

They’ve got good margins:

They’ve been able to reinvest in the business with high rates of return

They have no debt, and $62.75 million in cash on the balance sheet. When I looked at them, the market cap was about $165 million. Subtracting the cash means the whole company was available for about $102 million. Last year, they did $20 million in FCF.

The company was trading for 5x FCF, with 20% growth expected over the next few years.

Buybacks

According to management, Semler has spent about $5 million on buybacks recently, but they still have $15 million authorized and are considering more since they have so much cash on the balance sheet.

Before the recent run up, that would have let them buy back another 9% of the company. That’s significant, and if the board would authorize more buybacks, Semler could potentially take out a big chunk (25% or so) of their outstanding shares.

That looks way too cheap. Time to invert and find reasons not to invest.

The Issues

Changes in Reimbursement

The first thing I found was that the Centers for Medicare & Medicaid Services (CMS) implemented changes to the Medicare Advantage risk adjustment model in 2024. Specifically, they removed Peripheral Artery Disease (PAD) without complications from the model. This means that Medicare Advantage plans will no longer receive additional reimbursement for identifying patients with early-stage PAD. That’s bad news for Semler because QuantaFlo product is used for PAD screening.

Remember that QuantaFlo is the only product in the Semler catalogue.

It’s worth noting that Semler is applying to the FDA for approval to expand the conditions that QuantaFlo can be used to test for. They expect approval in the back half of this year. Management was very generic when asked what conditions they were expecting to get approval for. When asked directly in earnings calls, they said “heart dysfunction”.

Patent Expiration

In addition to Medicare phasing out payment for asymptomatic PAD screening, the patent on QuantaFlo expires at the end of 2027.

Recent Earnings

This is what caused the most recent steep drop in stock price.

Semler released earnings on May 7, and saw a drop of more than 25% in its share price the next day.

They missed EPS by 24%, announcing earnings per share of $0.78 for the first quarter, significantly below the average expectation of $1.03.

Revenue for the quarter declined 13% year over year, at $15.9 million. This number also significantly missed the consensus estimate of $21.4 million.

Net income did actually increase for the quarter due to declines in cost of goods sold and a reduction in SG&A costs.

Whatcha Gonna Do With All That Cash? All That Cash Inside Your Stash?

An analyst - the only analyst that follows the company asked just that. Here’s the transcript:

Aaron Wukmir:

“Okay. Understood. Appreciate all that color. And then obviously, you guys have developed and maintained a healthy balance sheet with a record cash balance this quarter. And you might have mentioned this a little bit in your prepared remarks, but have you had any conversations on any inorganic opportunities? I'd just love to get some more thoughts on potential uses of cash as we move forward throughout the year here.”

Renae Cormier (CFO):

“Sure. So really, when we're looking at our cash, there's kind of three areas that we're looking at: First and foremost is reinvesting back into our product. And so, an example of this is the heart dysfunction 510(k) clearance that we're going after. The second, as you mentioned, is inorganic growth activities. We do have a robust pipeline. But as you know, these things take time. So, we are going to be very diligent in what we're doing and what we're looking at.

Our Board has a lot of experience in capital allocation, and they are closely aligned with management and shareholders in trying to make sure that we carefully approach any acquisition that we may have. And then the third piece with our cash could potentially be share buybacks. So, we do have a $20 million share buyback that's authorized by the Board. We have bought back $5 million already, so we do have $15 million authorized in share repurchases.

So that's something else that the Board will obsess -- will assess looking at with capital allocation and depending on the market circumstances."

AAAND…. I’M OUT.

Let’s recap. We have a product that performs a test that Medicare is phasing out payment for. That’s a big deal. What Medicare does, other insurers follow.

Even if the test is clinically valuable and helps to screen for larger problems in the coming years, if it doesn’t get paid for, it’s not going to get done. Sorry patients, that’s just how things work.

Normally I’m not one to worry about some misses on revenue and earnings. But Semler is seeing declining revenue. When you couple that with the additional color of the reimbursement changes, well that starts to look pretty bad.

Especially when you consider that they have a single product in their portfolio, with 3.5 years to go on the patent.

Management is trying to spin the story of additional FDA clearances for “heart dysfunction”, but I don’t like the way they’re talking about this at all. They’re being very generic and have said in previous calls that people who are diagnosed using their technology will require additional testing. It’s all too fuzzy for my liking.

Then there’s the capital allocation. Reinvesting into the product is fine. But once they get the additional FDA clearance for additional testing, it’s just a software update to add that capability. How much money can that take?

#2 on the list was “inorganic growth” - read that as “we might buy another company.” Considering that Semler just wrote off $2.5 million for their acquisition of Insulin Insights, I don’t like this idea. At all.

#3 is buybacks. Given the low valuation, and high cash flow generation of Semler, this seems like the best use of cash. But I dug a little deeper here. The remaining $15 million they talked about having authorized for buybacks is from March of 2022.

I’m going to go ahead and bring a chart in here with a poorly drawn arrow at the point where Semler could have started buying back shares:

So your stock price has traded sideways at what looks like a cheap valuation for 2 years and you’ve spent 25% of your buyback authorization while building record levels of cash on your balance sheet?

Again, I don’t like this.

This looks to me like management isn’t confident in the future of their company. Perhaps because they’re a one-trick pony with limited time remaining and an uncertain future…

That was as far as I went with my research. This ended up in the “no” pile rather quickly.

Then Came This…

Semler Scientific Announces Bitcoin Treasury Strategy

“Semler Scientific, Inc., a pioneer in developing and marketing technology products and services to healthcare providers to combat chronic diseases, announced today that its board of directors has adopted bitcoin as its primary treasury reserve asset. In addition, Semler Scientific announced that it has purchased 581 bitcoins for an aggregate amount of $40 million, inclusive of fees and expenses.”

WHAT??

Your “pioneering” healthcare company spent $40 million - more than half of your cash - on bitcoin, instead of buying back your own stock?

Management believes in bitcoin more than they believe in their own company.

I feel pretty good about my analysis.

Their announcement did push the share price up by 40%. So, if you want to buy $40 million in bitcoin for $228 million and get a healthcare company that its own managers won’t buy in the deal, Semler might be a stock to look at.